The season of giving is upon us - the time of year when people make charitable donations before the end-of-year deadline for potential tax benefits. Tax law changes in recent years made these benefits more elusive for most people, yet there are still ways to do well both for yourself and your favorite charities with your donations.

You previously figured out your purpose for giving and how much to donate. Now, it’s time to execute. Depending on the amount and goals for the gifts, there is a range of strategies for donating money to qualified charities, those granted tax-exempt status by the IRS:

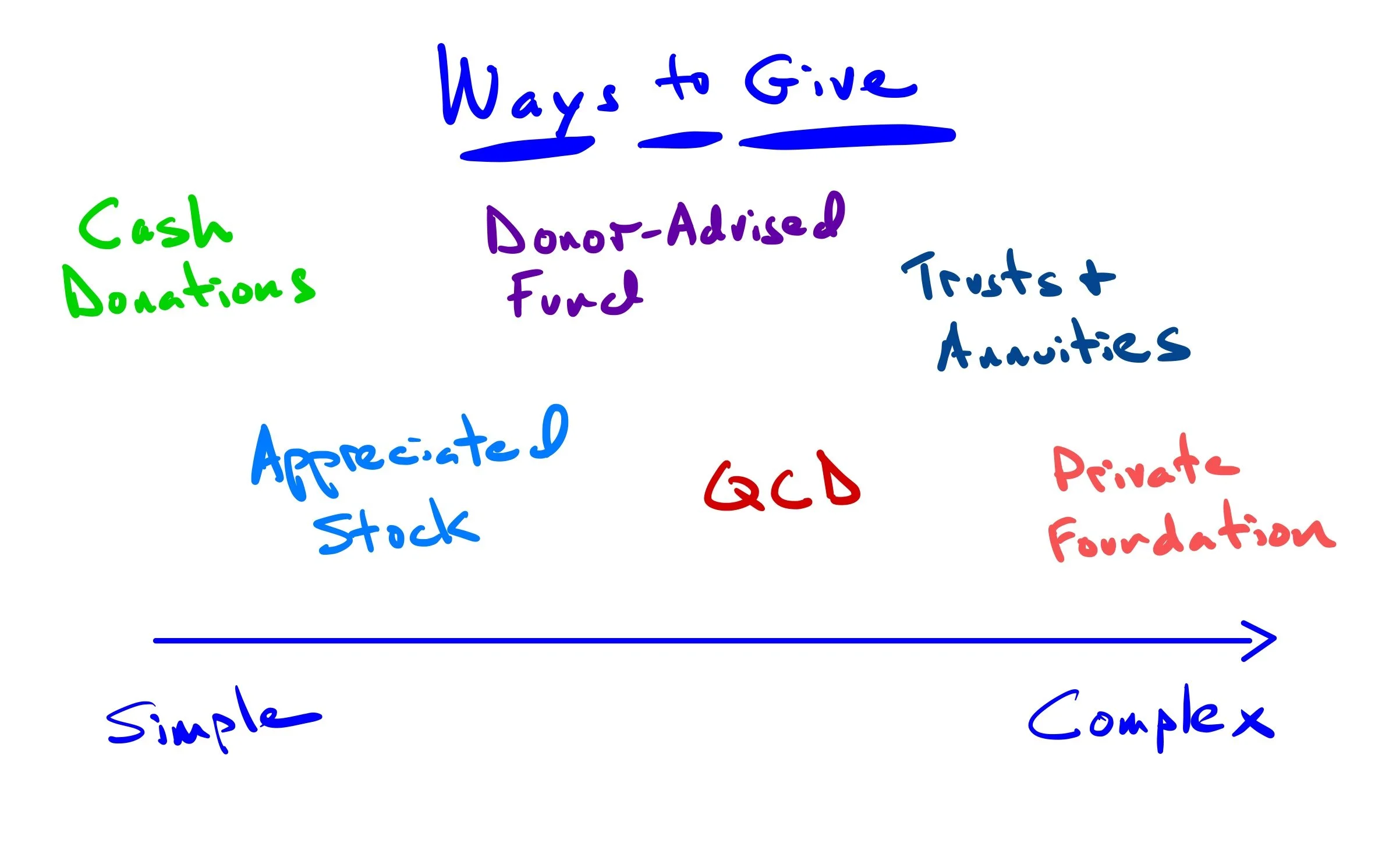

Cash Donations

You can send money directly with a check, credit card, or an envelope of cash (which we don’t recommend). If you don’t need a tax deduction for the donation, you’re all done - congratulate yourself for a good deed.

If you do want a tax deduction, you’ll need a receipt from the charity or some other documentation that you made the donation. To help with tax preparation later, you may want to keep a spreadsheet listing donations throughout the year, with amounts, dates and the names and tax ID’s of the recipients.

The spreadsheet will only be helpful for tax benefits, however, if you itemize deductions on your tax returns and your items add up to more than the standard deduction available to everyone. Tax-law changes a few years ago raised the standard deduction for everyone and limited the amount of available itemized deductions, so the number of people itemizing dropped from nearly 50 million to 15 million. Comparatively few people today are eligible to receive any tax benefit for their donations - something the charities themselves rarely highlight.

Depending on how much you donate, you may be able to receive at least some tax benefit by “bunching” your donations every other year or so. For example, waiting to donate $20,000 next year, rather than your usual $10,000 this year and next. Talk with your tax advisor to see if this might be a viable strategy for you.

Appreciated Stock Donations

Wouldn’t it be great if you never had to pay any tax on the investment gains with your stocks, bonds, or mutual fund shares? There’s a way: donate the appreciated securities to your favorite charities.

Since you don’t pay any taxes to donate the securities and the tax-exempt charities don’t pay tax to sell them, it’s a win-win for everyone (except the government tax coffers).

You’ll need to confirm that a charity is set up to receive stock donations (some smaller charities aren’t) and get their account details and transfer instructions. You’ll also need to instruct your financial custodian which investment and share lots to transfer and complete a form with other details such as the number of shares donated, purchase price, value at date of donation.

These kinds of complications prevent a lot of people who are charitably inclined from using this stock-donation method. Fortunately, there’s a way to simplify the process both for cash and stock donations by using one bucket for everything - a donor advised fund.

Donor Advised Fund

A donor-advised fund, or DAF, is a gift-fund account – often at major custodians like Fidelity, Vanguard and Schwab, or at a community foundation – where you can contribute assets for donation to charities later. You get an immediate tax deduction for contributing to the DAF and afterwards can donate to your favorite charities over time without having to worry about any further tax deadlines or the administrative details that come with direct donations.

The reason you get an immediate tax deduction for contributing to the DAF is that it’s managed by a sponsoring charitable organization, which now has legal control over the donated assets. This means that technically when you instruct the gift-fund to send money to your favorite charity, you’re “advising” the gift-fund to do so and it has discretion not to send the money.

In practice, this rarely happens as long as your designated charity is a qualified 501(c) organization, and if it is, but somehow isn’t on the gift-fund’s long list of just about every charity in existence, the fund will add your charity to the list after performing basic due diligence. As a result, it’s easy to use the DAF to send money to the shoe-string theater company operating in the storefront down the street as long as it’s a qualified charity.

Your donation can potentially grow, making available even more money for giving. Most sponsoring organizations have a variety of investment options from which you can recommend an investment strategy for your charitable dollars.

Many small charities aren’t set up to receive stock donations. A DAF solves this problem by receiving the stock from you and then sending cash to the charities.

You can use the DAF to donate to charities in your own name or anonymously – an easy way to keep yourself off of mailing lists.

You can also retire your spreadsheet, since most DAF’s have elegant client portals that show all the details regarding where you’ve given money over time, making it easy to repeat the process next year. You’ll also be able to give your tax preparer one number for the lump sum you donated to the DAF, rather than all the details for donations to multiple charities.

Instead of a mad dash to make your donations before December 31st, kicking yourself for having waited so long again, the donation process feels more like ordering online gifts for friends and family.

Some DAFs may require a minimum contribution to establish your own giving account and may also have minimum contributions and gifting requirements, so you should ask about them. At some funds, however, there is no initial contribution needed to establish one and with minimum gifting limits as low as $50, it's still easy to donate small amounts.

QCD - Qualified Charitable Donations

For people over the age of 70.5 who own a Traditional IRA, there is a particularly attractive strategy known as a “qualified charitable donation," or QCD, that involves donating money from the IRA to qualified charities.

This type of IRA distribution isn’t taxable, as it normally would be, and the donation amount counts toward any required minimum distributions (RMD’s). For people who do not need all of their RMD for living expenses, this giving strategy is a great way to reduce the amount of taxable income they would otherwise have. In turn, by lowering their adjusted gross income (AGI), they can avoid Medicare surcharges and the 3.8% surtax on net investment income.

In addition to needing to be at least 70.5, there are few restrictions to keep in mind with QCD’s:

- The maximum deductible contribution limit is $100,000.

- You must make IRA distributions directly to the charitable organization.

- The distribution must come from an individual IRA or a Roth IRA (although a SEP or SIMPLE IRA could also qualify if there are no active contributions).

- You can’t receive any benefit back from the charity for making the donation, so be sure to reject any tokens of appreciation a charity might want to give you to say thanks.

For more information, see A Tax Break Worth the Hassle. WSJ, Sept 21, 2023.

Split-Interest Gifts

These are typically complicated strategies requiring advice from accountants and attorneys and will not be helpful for most people. In short, a split-interest gift is basically one in which you keep part of the benefit while giving a charity the rest.

Charitable Annuities

- You make a gift to a charity and receive an income stream of guaranteed fixed annuity payments based on the gift amount. Some people like them because they reduce stock-market exposure and provide another source of income.

- The promised annuity payments are backed by the charity, however. While rare, there have been problems during tough economic environments like the 2008 financial crisis, so you’ll need to do your due diligence. (See Donors Find Gift Annuities Can Stop Giving, WSJ, May 12, 2009)

Charitable Trusts

- There are two basic types of charitable trusts - charitable remainder trusts (CRT) and charitable lead trusts (CLT). Both are complicated and will require financial and legal analysis to see if they’re right for you. Also, younger investors are typically precluded from using these trusts.

- With a CRT, you fund the trust with assets to generate an income stream for you or other beneficiaries, with the remainder of the donated assets going to charity. One advantage is the ability to sell an appreciated asset and diversify without paying capital gains tax.

- With a CLT, you fund the trust with assets to provide resources for a charity for a period of time – say, the life of one or more individuals – with the remaining assets eventually going to family members or other beneficiaries. Advantages include income-tax deductions or estate or gift tax savings on assets that are ultimately passed to your beneficiaries.

Charitable Pooled Income Fund

- A pooled income fund (PIF) is a type of trust that is typically created and maintained by a large public charity.

- In many ways, it’s similar to a charitable remainder trust, since the fund invests donations and distributes net investment income annually to each donor for life and distributes the remaining assets to charity after the donor passes away.

- One advantage: a pooled fund can accommodate younger investors and eliminate many of the implementation details that come with a trust.

Private Foundations

A private foundation is a charitable organization, typically established by an individual, family or corporation, to support charitable activities. These are complicated entities that require a board of directors or trustees to oversee receiving charitable contributions, manage and invest the assets, and make grants to other charitable organizations. They are also responsible for filing tax returns and other administrative reporting requirements.

A private foundation offers greater control over donated assets than other strategies such as donor advised funds. However, given the costs and complexity to administer them, some foundations have concluded that it’s better to dissolve themselves and transfer assets to a DAF.

****

In the end, there’s no one right way to donate to charity. Rather, you have a smorgasbord of options that can be used individually or together, and finding the best ones for you is as personal as deciding how much and to whom you’d like to donate.